Saving for the secure future of a child, especially a girl, is one of the most important goals for parents. While there are multiple investment avenues available for parents to achieve this goal, the finance minister, in the Union Budget, did his little bit for the girl child by making the Sukanya Samriddhi Yojana more lucrative. However, financial advisers still rate equities, particularly via the SIP route of mutual fund, as the best option to meet long-term needs.

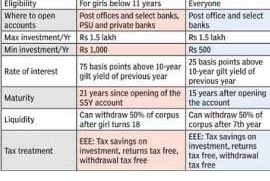

The finance minister allowed returns on investments in the Sukanya Samriddhi Yojana (SSY) as tax-free when withdrawn. This came in addition to the tax benefits already available for investments in this scheme under Section 80C of Income Tax Act. Post the Budget proposal, SSY will become an EEE investment, which means it will be classified as an “exempt, exempt, exempt” investment. An individual who invests in the scheme will get tax deduction, the income generated in the scheme will be tax exempt, and also when the person withdraws the corpus on maturity, that will also be exempt from any income tax burden.

There are some more investments which are classified as EEE type: Equity linked savings plans (ELSS), Public Provident Fund and life insurance policies. Tax-saving FDs and NPS do not fall in this category and are categorised as EET – there is a tax burden when one withdraws the maturity corpus.

After the budget, comparisons have been made between SSY and PPF, both EEE-type investments. More so because SSY offers a higher rate of interest than PPF. While the rate of return in PPF is 25 basis points (100 basis points = 1 percentage point) over the 10 year gilt (government bond) yield of the the previous financial year, SSY offers returns 75 basis points over the 10-yeear gilt yield. Thus, in effect, SSY gives the investor 50 basis points higher return than PPF.

According to Mrin Agarwal, who runs Womantra, a financial awareness programme for working women, keeping aside the rate of return, PPF still scores over SSY. “In case of PPF, you can withdraw funds, you can take a loan and after the first 15-year period, you can extend it for 5–year periods. One should use PPF to build a retirement corpus,” Agarwal said. In comparison, “Sukanya Samriddhi Yojana should be used for meeting expenses relating to higher education and marriage of a girl child. Also it should be compulsorily closed after 21 years,” she said.

Is there a better investment option for the girl child? According to Agarwal, for securing the financial future of your girl child, a systematic investment plan (SIP) in a good equity fund “is the best option”. However, one of the main things to take care of while putting in place a financial plan for your child is the number of years remaining before she will need the money for her higher education or for her wedding.”If she is 5-6 years old, and the time for her to go for higher education is at least 10 years hence, one should invest in an equity mutual fund,” Agarwal said. However, if your goal is short term, that is the time left for you to spend on her education or wedding is about 4-5 years, “one could go for a debt mutual fund or a balanced fund,” she said.

Other than these two investments, financial planners also advise their clients to have a pure term policy for the main earning member of the family. This will ensure that the child’s future education or wedding may not be disrupted even if the main earning member in the family is no more.

Also in most Indian families, the child is given money during major occasions and festivities. Financial planners suggest that rather than spending such funds, all monetary gifts that the child receives should be invested in the child’s name, preferably in equity mutual funds. This is because most parents take care of the necessities of their child. So spending those extra funds on the child itself may not be necessary. Rather investing those funds in a good mutual fund would be a wise decision for the long-term financial future of the child. This is because occasional inflows in those funds, over several years, is almost sure to leave a large corpus when the child grows up, they say.Agarwal also had more advice for parents willing to put in place a financial plan for their child.”One should not put money in fixed deposits for a child’s future. One should not also put money in child’s policy for the same. In these investments, returns are not very high,” she said.

How to open SSY account

A Sukanya Samriddhi Yojana account may be opened in a post office or branches of some designated banks by her guardian in the name of the girl child. From 2016, an account could be opened before the girl turns 10 years. Only for the current year, this age limit is 11 years. You need the girl’s birth certificate, address proof and identity proof to open the account. The initial deposit is Rs 1,000, after which any amount in multiples of Rs 100 could be deposited with the maximum deposit in a financial year at Rs 1.5 lakh.

Original Source:

*Photo credit: Times Of India

Source: Article written by Partha Sinha in Times Of India on Mar 24, 2015

Original article link: https://timesofindia.indiatimes.com/business/india-business/Equities-best-bet-when-saving-for-girl-child/articleshow/46670541.cms