In an overall financial literacy survey carried out by MasterCard, called the MasterCard’s Index of Financial Literacy, India ranks the lowest in basic money management skills among Asia-Pacific countries( source: Moneylife – Aug 2013).

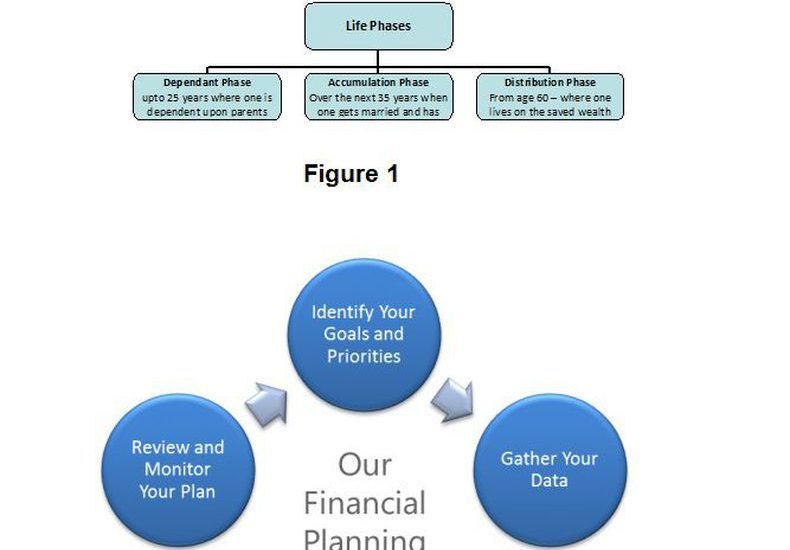

Before we start to manage our monies it is important to understand which stage of life we are in. Broadly the stages are classified Figure 1 above.

Once you are aware of the phase you are in you must prioritise and be clear on your financial goals.In many of our programs conducted, we came across people who want to save but don’t have a specific goal in mind for saving. The issues with not saving for a goal is mainly associated with investing randomly which can lead to

1) Wrong investment – tendency to choose current fancy

2) Wrong timing – People tend to buy at peaks and sell at lows

3) People tend to invest for short term

4) People are not able to gauge the amounts required for long term goals

It is imperative that we plan for all phases well with a goal, while in the accumulation phase plan for now and for the distribution phase. For this we need to do proper financial planning.So what is Financial Planning?

Financial planning is the process of examining one’s personal situation, financial resources, financial objectives and financial problems in a comprehensive manner, developing an integrated plan to utilize the resources to meet objectives and solve problems and monitor the plan performance to take corrective action as necessary to meet the plan projections.

Although this may sound daunting, it is nothing but a simple exercise about allocating your monies to achieve future goals. Everybody needs financial planning irrespective of their wealth.

Before you make a financial plan, ask yourself a few questions to assess your position on the understanding of your finances-

1. Do you know the household budget? Do you have an expense tracker?

2. Do you have emergency savings and if so, how much?

3. Are you aware of your savings and who selects and manages your investments?

4. What are your financial goals and have you planned for them?

5. How have you planned to pass on your financial legacy?

The journey of the Financial Plan is extremely simple. Follow these 4 simple steps to reach your financial goals.

Step I – Current financial situation.

For this you would need your income details and estimate of expenses (including outflow for EMIs, insurance premiums). The difference in the two will give you the surplus available for investing monthly.

Step 2 – Identifying Goals

The goals for which you wish to save. Goals must be specific, measurable, time bound and realistic. Goals could be long term for e.g. retirement, children’s education or short term like saving for the down payment for a housing loan. Goals could also be as simple as trying to invest on a regular basis to build a nest egg which could be used for other lifestyle needs like foreign vacation etc. Goals should cover 3 main horizons:

Short Term Goals – upto 1 year (Holiday, Liquid Funds,)

Intermediate Goals: 1-10 years (Childrens Education, Purchase of House)

Long Term Goals- > 10 years (Retirement Planning)

Once you have an idea on the goals you wish to save for, you action your financial journey by creating a financial plan. Don’t wait until a money crisis to begin financial planning. The earlier you start the better off you would be in the long term. If you are investing for the first time on your own, start small, understand and then invest. Learn where others have invested for you (what kind of products your husband/father has invested in.) You can use freely available tools and calculators on MF websites to get an idea on how financial planning works. Or you can take the help of a financial planner who can create and review financial plans.

Step 3- Choosing Products

You choose products which match your goals. There are many simple products available like fixed deposits, public provident fund, post office schemes, mutual Funds and insurance Products including medical Insurance. Learn the basics of these products. Most importantly, understand the risk associated with each of these investment avenues.

The internet is an ocean of information on any of the above subjects. The Indian mutual fund websites have very good articles for investor education. Other websites compare insurance policies. Use these to check on various insurance policies. Attend financial education programs, which help you understand the above from a practical aspect.

Some products like PPF can be used for retirement planning and Mutual Fund SIPs can be used to plan for children’s education. It is also important for you to assess your risk taking ability and invest accordingly. For this you must undertake a risk questionnaire. It tells you your ability to take risk- however your willingness to take risk may be higher or lower. But it is important to understand your risk profile and allocate your assets accordingly.

Couple of points to be kept in mind while choosing products:

1) Don’t buy on tips, impulse or left behind feeling

2) Don’t chase last year’s topper

3) Stick to your asset allocationStep 4 – Review Your Portfolio

Finally, you must regularly review your portfolio. There are many free portfolio trackers available online on which you can upload your portfolio. These trackers give you the returns on each of your investments. At the end of the year, see how much different investments in your portfolio have helped you reach your goal it is a good idea to have a yearly financial audit for this purpose. The audit will also throw up underperforming investments.

Financial Planning Hygiene Factors

Couple of things to keep in mind on your plan:

1) Don’t force yourself to track every rupee

2) Remain positive about your plan – don’t view it as a punishment

3) Don’t lose sight of your plan

4) The plan should withstand minor setbacks

Hence the plan developed must be flexible in case goals change and provide protection and liquidity easily. Plans must also be tax efficient.

You must realise that financial planning is actually a journey of your financial life and the journey fructifies only if you stick to your financial commitments and action out the advice given by planners. Many times, people go through the stage of getting financial plans written but then do not action them out. We have also seen many people confused by multiple page financial plans, so remember to have a one page plan which is actually enough to cover your financial life.

Womantra TIPS on what women must focus on while planning:

Know How much to Save – A 2012 study by the US-based Putnam Research Institute says that the fund selection, asset allocation and portfolio rebalancing do not not impact the final portfolio as much as the quantum of savings. Hence it is very important to start saving at least 40% of your take home.

Start Early – Most of us do not think about retirement till our late thirties. The actually planning begins when we are nearing 50 and have just ten odd years to save.

Mrin Agarwal & Rima H

Founders and Trainers Womantra

womantraining@yahoo.com

Womantra Facebook Page

Original Source:

Source: Article written by Mrin Agarwal and Rima Hinduja in Sheroes.com

Original article link: https://sheroes.com/articles/steps-to-reach-your-financial-goals/NDM2